Why Lay Hong appears dismal after posting record earnings?

Billy Toh

/

The Edge Financial Daily

May 02, 2019 09:55 am +08

KUALA LUMPUR: It was barely a year ago that poultry and eggs firm Lay Hong Bhd posted record earnings for its financial year ended March 31, 2018 (FY18). At the time, its shares were trading close to RM1 apiece. Since then, its financial performance, together with its share price, has dived.

Based on the closing price of 45 sen a share on Tuesday, Lay Hong’s shares has halved from the 92 sen they settled on April 30, 2018, as the group turned in disappointing financial results each quarter in the nine months after FY18 concluded.

A fund manager who has placed money on Lay Hong said it was a classic “over-promise-under-deliver” situation, and that many institutional funds have been left disappointed by the group’s financial performance. Among the funds which have since exited Lay Hong were Kenanga Unit Trust Bhd, Great Eastern Life Assurance (M) Bhd, and Libra Invest Bhd.

Advertisement

But were there signs that indicated a deterioration was to be expected? Some say there have been some concerns about certain numbers. A look into Lay Hong’s financials showed there has been notable increases in its biological assets, inventories and receivables in the past three to four years.

Compared with FY15, its biological asset rose 53% to RM39.96 million in FY18, while inventories climbed a notable 39.9% to RM91.7 million from RM65.5 million. Trade receivables, meanwhile, has more than doubled to RM141 million in the same period.

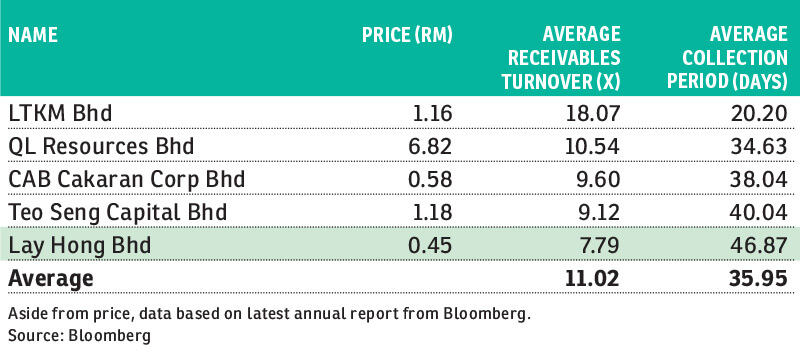

While these assets grew concurrently with the group’s revenue and expansion, it is worth noting that Lay Hong’s average receivables turnover stood at 7.8 times, which is much lower than the industry’s average of 11 times.

Average receivables turnover is the number of times per year a business collects its average accounts receivable. The ratio is used to evaluate a company’s ability to efficiently issue credit to its customers and collect funds from them in a timely manner. A low receivables turnover ratio might be due to a group having a poor collection process, bad credit policies, or it has more customers that are not financially viable or creditworthy.

When asked about these, Lay Hong’s executive director Yap Chor How told The Edge Financial Daily that the cost increase the group has had to face “has led to the cost capture in the inventory to go up”. “There was also an increase in capacity on our end. Thirdly, inventory on the supermarket level has also gone up.”

As for its receivables that has more than doubled in the last three years, Chor How said the group’s revenue had also more than doubled in the same period to RM847.8 million in FY18 from RM671.7 million in FY15.

While it is true that the revenue growth has been impressive, other poultry players such as CAB Cakaran Corp Bhd, which has similarly seen its revenue double during the same period, has a higher average receivable turnover of about 9.6 times, compared with Lay Hong’s 7.8 times.

Lay Hong’s average collection period is 47 days, which is longer than the industry’s average of 36 days. Prior to this, the group’s average collection period was below 40 days — it was 34 days in FY15.

An industry observer is of the opinion that the sharp increase in the receivables and inventories should be viewed as red flags. Coincidentally, it happened following the emergence of Chin Boon Long, who is known as a savvy investor, as one of Lay Hong’s substantial shareholders — albeit for a short period — in 2015. And whether it was another coincidence or not, Yap Hoong Chai, the group’s founder, was seen acquiring substantial stakes in some companies said to be linked to Chin, just weeks before Chin bought into Lay Hong.

Better egg prices anticipated to lift bottom line in FY20

Chor How, however, dismissed concerns about the group’s rising inventories and receivables, adding that most of Lay Hong’s customers have trading terms of about 60 days on statement, and a maximum of 90 days. “The more [business] we do, the more receivables we have. But these (clients) are good paymasters,” Chor How added.

Chor How also believes that the group is on track to record a better financial performance in FY20, on anticipation of a recovery in egg prices.

“From what I see, the price impact only started to be reflected in our third quarter. The full impact of better pricing is likely to be seen in the fourth quarter [of FY19], the first quarter of the upcoming financial year, and the preceding quarters,” he said.

Hence, management, said Chor How, is confident that the group can “easily” improve in terms of its bottom line.

This was because he said the last three quarters’ weaker financial results were mainly due to lower egg prices, as well as prudent measures Lay Hong undertook to prevent the bird flu virus that was detected, by the Sabah veterinary department near one of its farms in Tamparuli, Sabah, from spreading further.

“What happened to a lot of farms, including us, was that we had to reduce our production by not bringing in new livestock. So, our production dropped. We should be working about 2.5 million eggs [per day] in West Malaysia but we reduced it to about 2.1 million eggs [per day], about a 10% reduction. To bring production up again, it will take about six to seven months,” Chor How said.

Altogether, Lay Hong’s overall production fell from three million eggs per day to two million eggs as the group also lowered production elsewhere due to lower egg prices.

Chor How expects other companies’ farms will also raise their production now that egg prices are recovering, adding that the industry is expecting prices to stabilise in the near future.

“We foresee stabilised pricing in the near future because of a few reasons. [Firstly,] the disease issue, which will continue to affect the farms that are infected. From what we see, it will take time for these farms to recover their production. So, we foresee the recovery will take about a year. Even if prices are to drop with more production, we think it (prices) will still be relatively stable,” he said.

Another reason he cited is higher feed costs, which most producers have adjusted into their pricing. Chor How said egg per production cost rose to about 28 sen recently from 26 sen in the last one to two years as feed costs have increased. But with feed prices stabilising, most producers have adjusted the higher cost into their pricing.

To Lay Hong, Chor How said the challenge is in supplying eggs to both the open market and fixed market, as prices of eggs in the latter take longer to adjust. The group supplies 50% of its eggs to the open market and the other half to the fixed market.

While Chor How is brimming with confidence, there appears to be more sceptics than believers at this juncture, going by the group’s share price movement.