If you have this stock, really cry also no tears.

Bumi Armada’s shares dive 21%

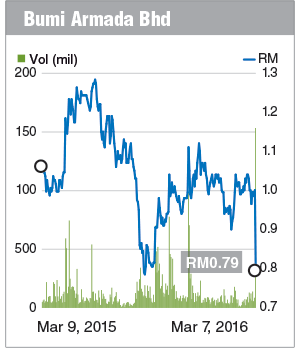

KUALA LUMPUR: News on termination of a charter contract for its floating production storage and offloading (FPSO) unit sparked heavy selling of Bumi Armada Bhd shares, which dived 21% or 21 sen to a six-month low of 79 sen yesterday.

Termination of contract by its client, Woodside Petroleum Ltd (Woodside), is expected to deal a big blow to Bumi Armada’s financials considering the demand for assets, like FPSO, is weak in the current severe downturn in the oil and gas industry.

Bumi Armada owes some US$198 million (RM805.82 million) to a consortium of banks for the financing of the FPSO, according to sources familiar with the matter.

“Bumi Armada would be in a more difficult situation as it is much harder for the group to look for another FPSO client under the current oil price scenario which provides similar return on assets as implied by t he original contract,” said Hong Leong Investment Bank Research.

The Edge weekly reported that the region’s leading FPSO operator is currently under pressure from the consortium of banks, including Sumitomo Mitsui Banking Corp and France’s Natixis, which has lent it money to finance the FPSO, called Armada Claire. The unit has been operating at the Balnaves oilfield, offshore of northern Australia since first oil delivery in August 2014.

While Bumi Armada seems to be looking to fight the termination, but with the compensation remaining unknown, most analysts are revising their target price on Bumi Armada shares.

“This turn of events was a negative surprise and is likely to weigh on sentiment for the stock. It could also raise concerns for other existing contracts. We downgrade from ‘add’ to ‘hold’,” said CIMB Research, which has downgraded the stock to “hold” from “add”.

Kenanga Research has also downgraded to “underperform” from “outperform” on Bumi Armada with a lower target price of 80 sen, while JF Apex has also downgraded the stock to “sell” with a target price of 90 sen.

According to JF Apex Securities analyst, Lee Cherng Wee, the notice of termination from Woodside is an unexpected cancellation.

When asked if the stock price is oversold, Lee said it could be a knee-jerk reaction to the news. “However, we are concerned on the possibility of more cancellations of its prized FPSO contracts in view of the ailing oil and gas sector,” he added.

An analyst from Public Investment Research agreed that the revision on the target price is an overreaction.

“Like all oil negative or adverse oil news, it is definitely a knee-jerk reaction in terms of the magnitude of the news. We still need further details to fully assess the project,” said the analyst.

Public Investment Research has previously questioned the potential contract extension of Armada Claire, after channel checks about depleting production coupled with lower oil price that could severely impact the commercial viability of the Balnaves field.

“We had therefore assumed the non-extension of the option and also excluded the project from our FY16 (financial year ending Dec 31, 2016) onwards valuation. Our target price of 90 sen premised on our DCF (discounted cash flow) valuation is thus retained.” It added.