Personally I have ARMADA and DELEUM. ---- KANASAI STOCK, LOSS KAW KAW.

This article first appeared in The Edge Financial Daily, on February 10, 2020.

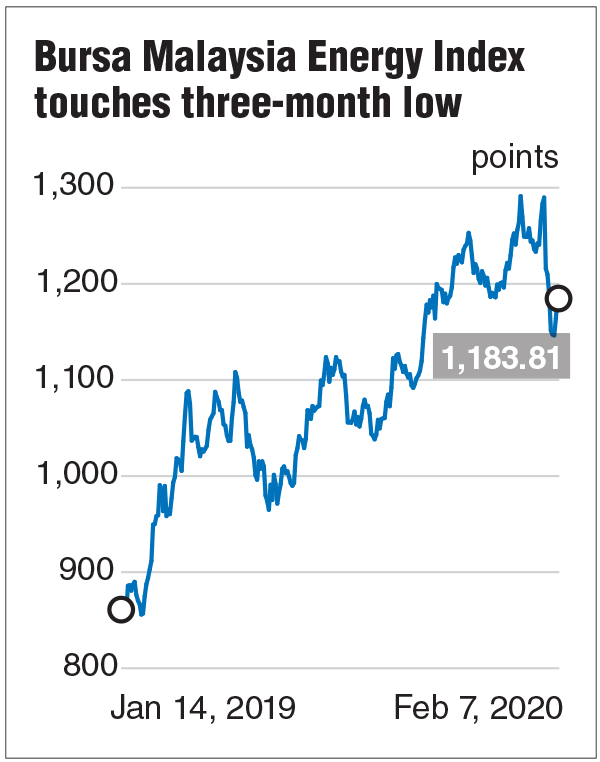

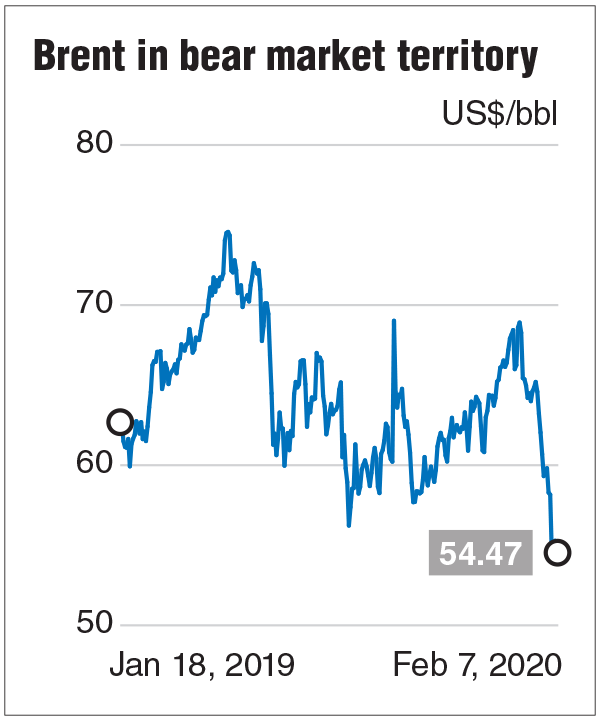

KUALA LUMPUR: Shares in oil and gas (O&G) companies fell to three-month lows last week as oil prices slipped into bear market territory.

The Wuhan virus outbreak sparked concerns over demand for the commodity, putting on pause the sector’s one-year rally on Bursa Malaysia that was driven by better earnings and job prospects.

Attention now will be on the soon-to-be released quarterly corporate earnings, an analyst told The Edge Financial Daily.

“Stock sentiment ran ahead of fundamentals last month,” said the analyst. “[Shares in] those that deliver bad results will not run.”

The Bursa Malaysia Energy Index is still up 34.5% year-on-year, with historical price-earnings ratio (PER) of 22.36 times despite the recent pullback.

The analyst said that valuation of around nine to 12 times PER “makes sense” to companies which are gaining traction but suffered some setbacks during the O&G industry downturn.

Room for gains after 2019 rally

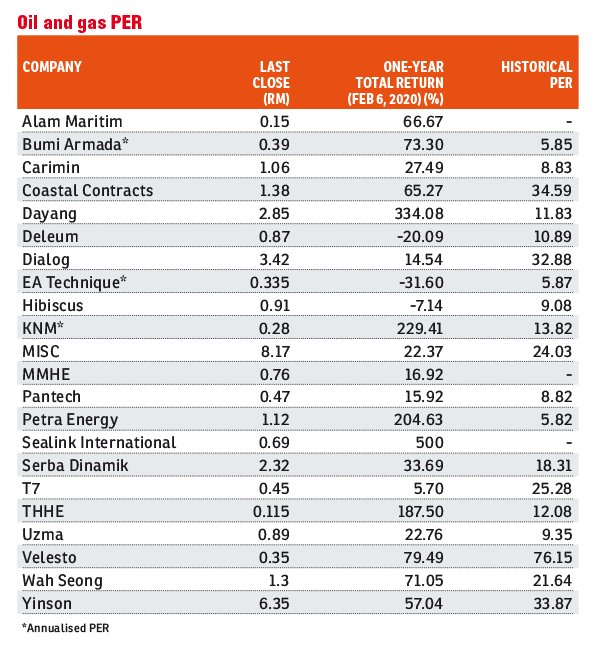

Of the 20 O&G companies observed by The Edge Financial Daily, nine are trading below the low 12 times PER benchmark, suggesting that there is room for gains. Of course, each company has a different story to tell.

They include hook-up and commissioning (HUC) services providers like Carimin Petroleum Bhd and Petra Energy Bhd, which have seen their share prices doubled from their 2019 lows, thanks to consistent profits for five quarters and four quarters respectively. Carimin is trading at 8.83 times PER, while Petra Energy is at an even more attractive 5.82 times PER.

Their peer, Dayang Enterprise Holdings Bhd, whose share price quadrupled in 2019, is now trading at a trailing 12-month PER of 11.83 times.

There is some resistance amid concerns that HUC jobs in 2020 will slow by 27% year-on-year based on Petroliam Nasional Bhd’s (Petronas) Activity Outlook.

Dayang’s forward PER stood at 15 times.

It has been pointed out that the stellar 2019 performance was due to higher HUC activities that was beyond Petronas’ previous estimate.

On another note, these companies may benefit from the slew of maintenance, construction and modification jobs coming in — although at slightly lower margins, analysts pointed out.

Dayang is en route to complete its second consecutive year of profit.

Meanwhile, KNM Group Bhd, whose share price gained 400% in 2019 on the back of three profitable quarters after three years of losses, is now trading at a PER of 13.8 times.

Separately, some see more room for gains for Petronas-linked shipping group MISC Bhd, which was the FBM KLCI’s second-best performer in 2019 in terms of share price with a 30% gain.

MISC has just secured a RM2.16 billion vessel project in Brazil. It is also bidding for floating asset projects worth over US$2.5 billion (RM10.35 billion) combined. Its share price is currently trading at RM8.17, against the consensus target price (TP) of RM8.82.

Meanwhile, rig operator Velesto Energy Bhd, whose share price doubled in 2019, is expected to deliver higher core earnings in 2020, thanks to the current hot market.

Of Velesto’s seven rigs, one has a firm contract, while four have extension options. Velesto also has two of its five hydraulic workover units in charter. Analysts’ TP for Velesto averaged 45 sen, versus its last close of 35 sen.

On the other hand, rotational play could bring undervalued counters to the market’s attention. Sector laggards include vessel operator EA Technique (M) Bhd, piping company Pantech Group Holdings Bhd, well expert Uzma Bhd and oilfield services group Deleum Bhd.

EA Technique is en route to register high earnings growth after its capitalisation exercise which is slated to complete this year.

The full impact of Pantech’s resumption of carbon steel shipments to the US will be felt this year, while Uzma is a strong contender for the increasing well plugging and abandonment activities in Malaysia.

As for Deleum, it posted better-than-expected power and machinery segment earnings in the last quarter, although the growth story appears limited for now.

Otherwise, three stocks remain analysts’ favourites due to their stellar track records, earnings growth prospects and strong management.

Floating production storage and offloading operator (FPSO) operator Yinson Holdings Bhd, which has an average TP of RM8.27 against its last close of RM6.35 thanks to a slew of huge contract wins to secure long-term income.

Tank operator Dialog Group Bhd with assets to sweat out in Pengerang, Johor, has a consensus TP of RM4.05, against its last close of RM3.42.

Engineering firm Serba Dinamik Holdings Bhd has an average TP of 2.76, against its last close of RM2.32 — trading at a comfortable 15.3 times forward PER estimates.

Upside priced in for select counters

Another company with strong turnaround story, Sapura Energy Bhd, has yet to fetch an upward rerating, mainly because pundits insist on seeing profit first, which is expected to normalise sometime next year.

Despite an order book of over RM15.1 billion last year, Sapura Energy’s consensus TP remains at a low 32 sen due to slower-than-expected turnaround. The counter last closed at 24 sen.

Exploration and production outfit Hibiscus Petroleum Bhd has boasted continuous efforts to increase crude oil production efficiency. Its forward PER stood at 6.07 times — but sentiment is mixed as its earnings are closely affected by oil price movement.

Others appear to have already priced in potential upside.

Analysts are mixed on vessel operator Bumi Armada Bhd, which has seen its share price jump 242% in 2019. Currently showing an operating profit with an attractive financial year 2019 estimate of 5.85 times PER, Bumi Armada’s valuation hinges on its ability to clean up its balance sheet. Its TP ranges from 20 sen to 75 sen, with an average 52 sen, compared with its last close of 39 sen.

Bumi Armada has yet to announce a successful recategorisation of its RM1.47 billion short-term debt under Armada Kraken to long-term debt, which it previously expected to do by end-2019.

“We continue to work with the lenders to complete the process,” a spokesperson for Bumi Armada said in an email reply to The Edge Financial Daily.

“The company may provide an update once it is completed, if it falls outside our quarterly reporting schedule.”

Another headache for Bumi Armada is the failure of its US$275 million claim against Woodside Energy Julimar Pty Ltd for wrongful termination of a contract in 2011. Bumi Armada is filing an appeal against the decision.

Analysts are not discounting further impairment on its assets if the status quo remains.

Another vessel player, Alam Maritim Resources Bhd, last closed at 15 sen — double its 2019-lows — on the back of its first profitable quarter after two years. But it needs to recapitalise its balance sheet, being cashflow negative with short-term liabilities of RM144.17 million at end-September last year. It just proposed two private placements of 30% its share base to raise a minimum of RM48.29 million for working capital purposes.

Piping expert Wah Seong Corp Bhd gained traction with an attractive order book of over RM900 million, and is a potential beneficiary of future piping-related works for FPSO players. However it last traded at RM1.30 versus the consensus TP of RM1.22. At last close, it is trading at 16.46 times forward 12-month PER consensus estimate.

Malaysia Marine and Heavy Engineering Holdings Bhd, which is in a net-cash position and has an orderbook of RM2.7 billion, last traded at 76 sen against its consensus TP of 92 sen. Some analysts suggest to wait for a turnaround in its bleeding heavy engineering segment.

Too early to gauge Wuhan virus impact

Seasonally, the fourth quarter is weaker for Malaysian O&G companies because of the monsoon season. But company chiefs have been quoted in news reports saying that work activities persisted in the fourth quarter of 2019, which could translate into better-than-expected results.

The better results would justify higher prices for the stocks currently dogged by low valuation multiples.

It is too soon to gauge the impact from the Wuhan virus outbreak on global growth and oil demand, as it has yet to reach its peak, now with over 30,000 infected across 28 countries, and death toll nearing levels seen during the outbreak of the severe acute respiratory syndrome in 2003.